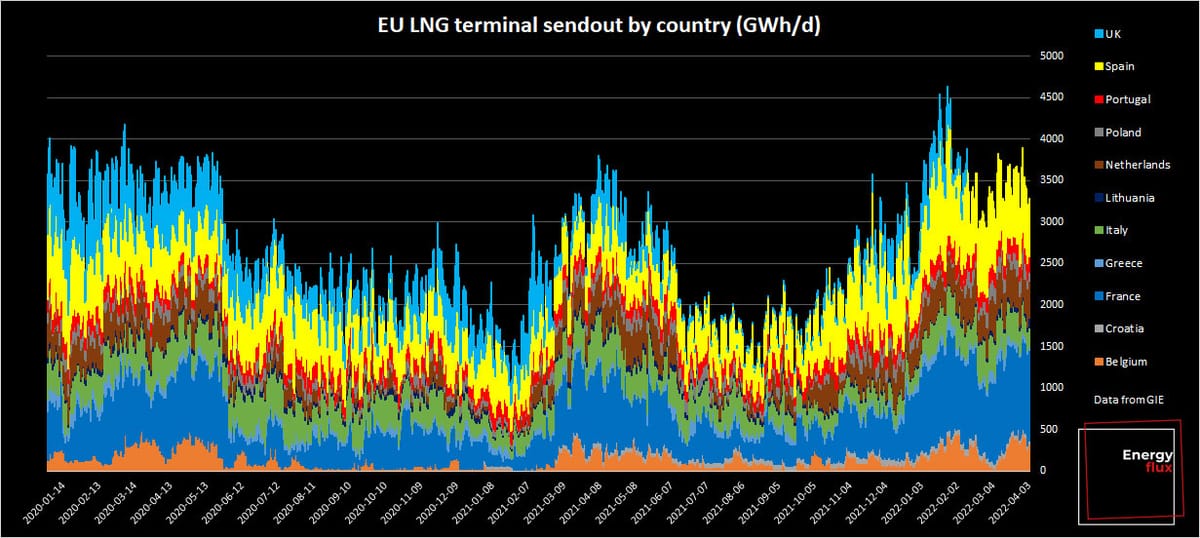

Infrastructure overkill?

Rush to build out EU LNG import capacity seems a bit flawed

Member discussion: Infrastructure overkill?

Read what members are saying. Subscribe to join the conversation.