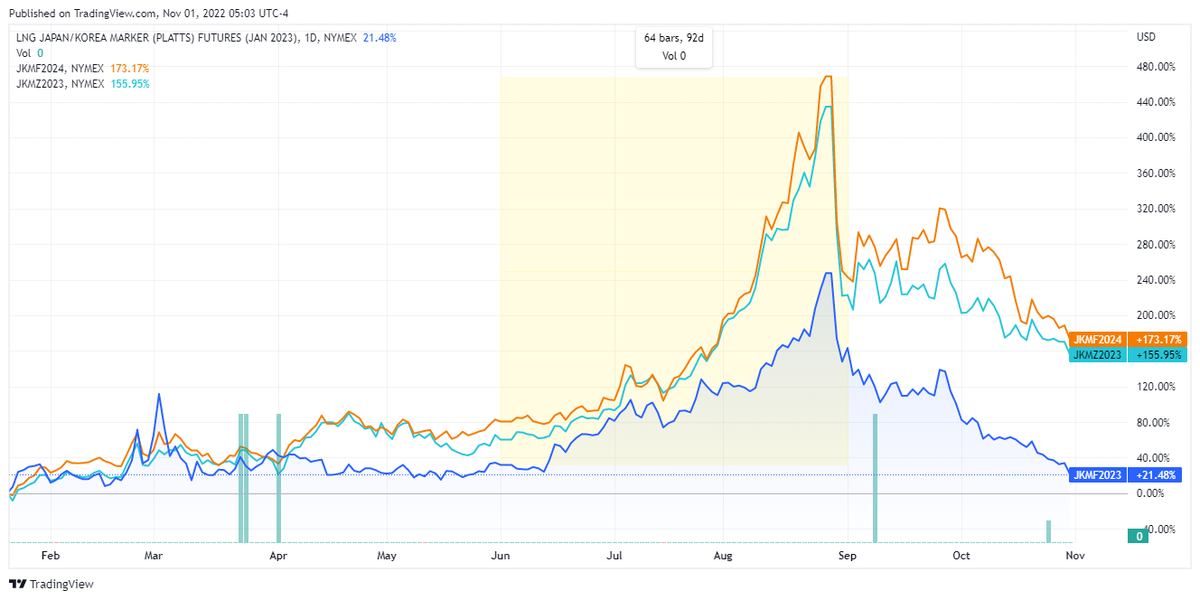

HOT TAKE: BP’s LNG hedge turns sour

But ‘exceptional’ gas trading propels earnings

Member discussion: HOT TAKE: BP’s LNG hedge turns sour

Read what members are saying. Subscribe to join the conversation.