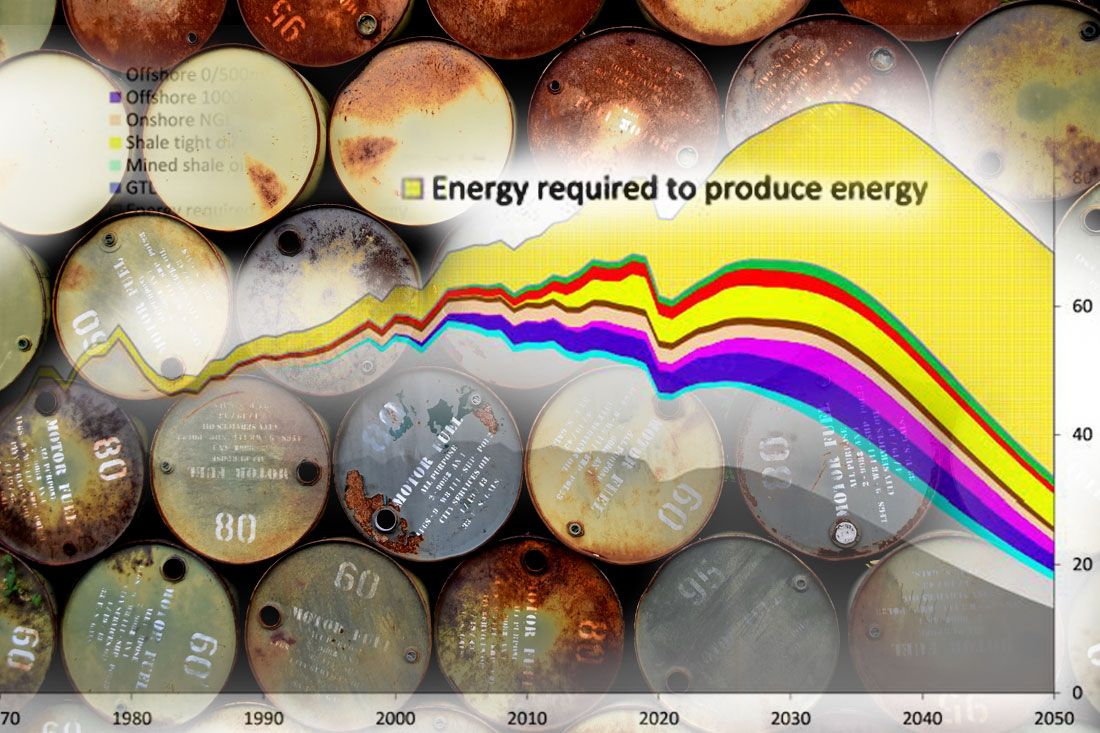

Scraping the barrel

DEEP-DIVE: We need to talk about energy return on energy investment (EROI)

Member discussion: Scraping the barrel

Read what members are saying. Subscribe to join the conversation.