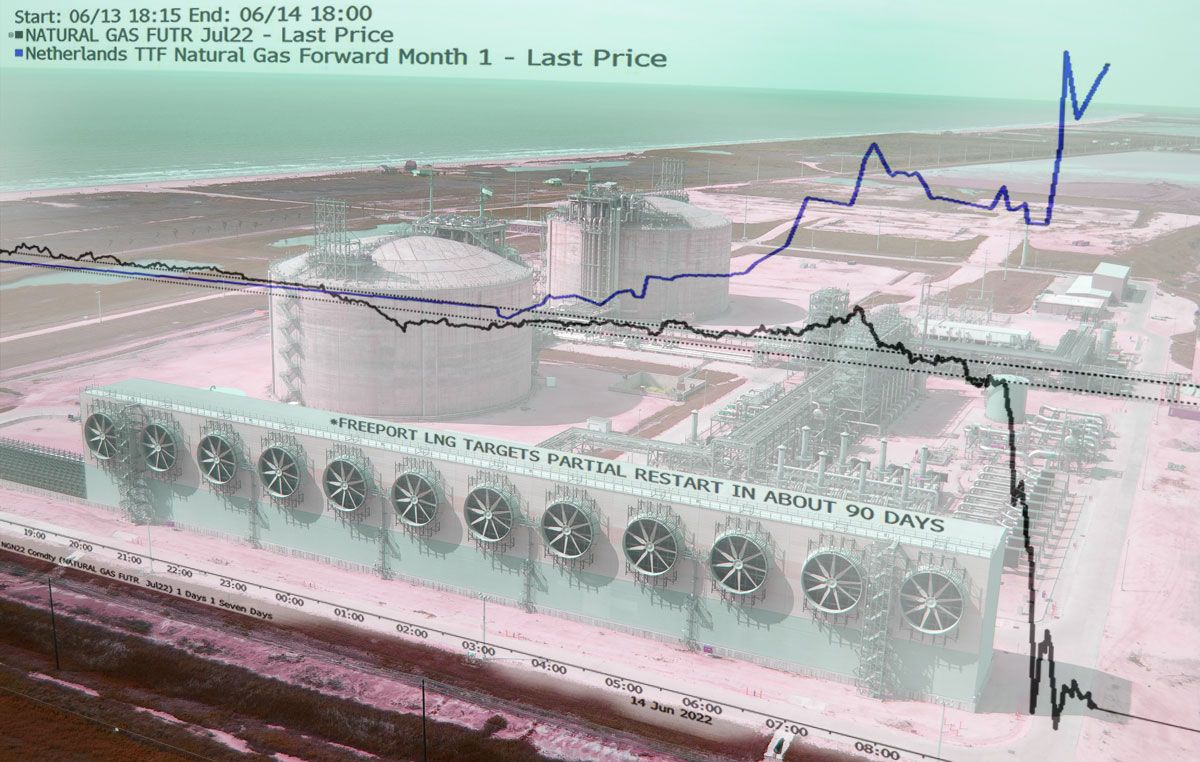

US LNG is becoming a zero-sum game

More American gas in Europe means more price pain for American consumers — and vice-versa

Member discussion: US LNG is becoming a zero-sum game

Read what members are saying. Subscribe to join the conversation.