When the dam breaks

CHART DECK: It never rains gas, but it pours LNG

The global liquefied natural gas glut has arrived. The thin end of the wedge of new LNG supply is manifest in key datapoints – yet commodity markets are still not fully pricing in this dawning physical reality.

The confluence of indicators pointing towards a sustained loosening of global gas balances is becoming overwhelming. All signs point the same way.

Whether you’re looking at North American LNG supply growth, cratering Chinese demand, investment fund short-buying, or Russia’s defiant LNG diplomacy, the message is the same: the gas glut cometh.

With the commissioning of Plaquemines LNG, ramp-up of LNG Canada, and Golden Pass inching towards first LNG in Q4, an unprecedented supply wave is breaking in slow motion over global energy markets.

Russia emboldened

Adding to the deluge is a Nobel prize-seeking American president apparently turning a blind eye to the return of sanctioned Russian LNG.

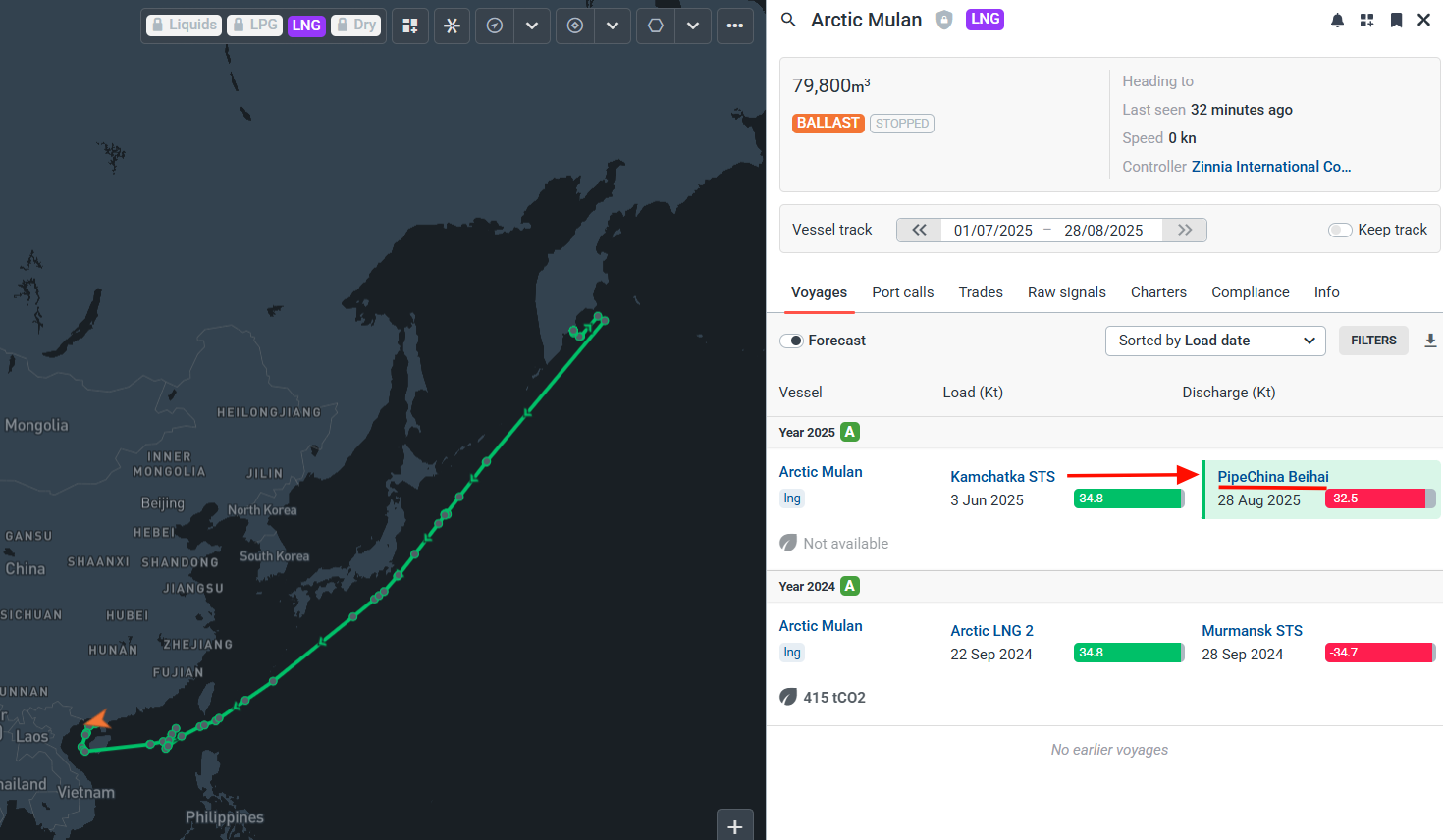

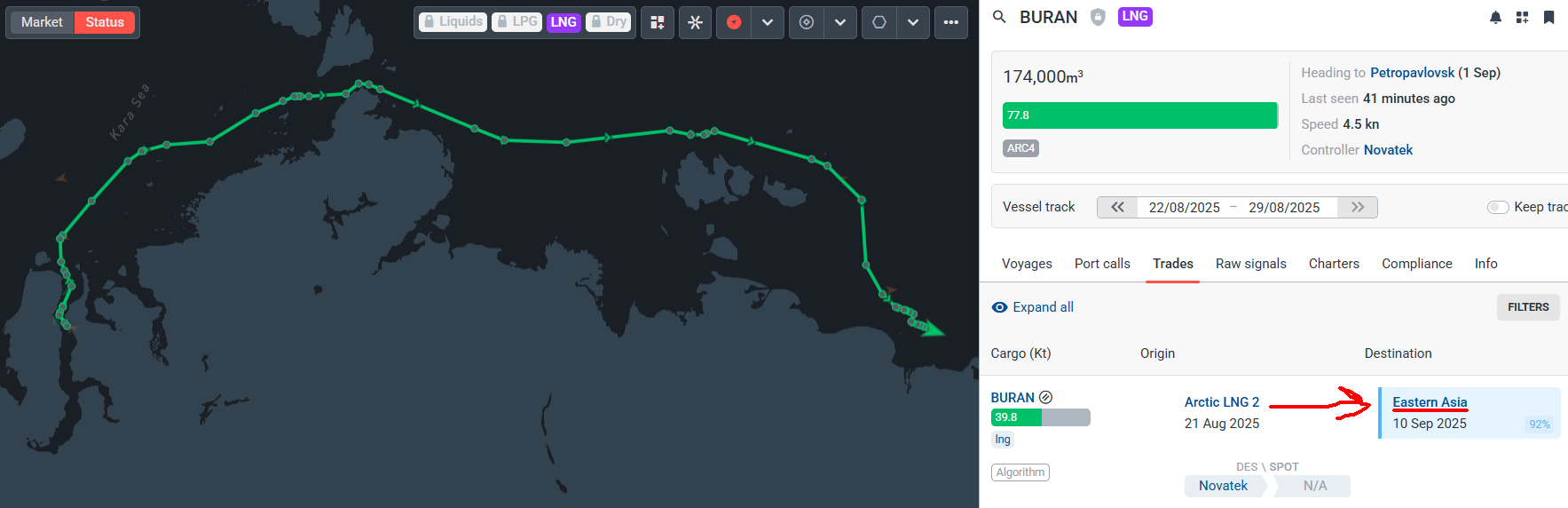

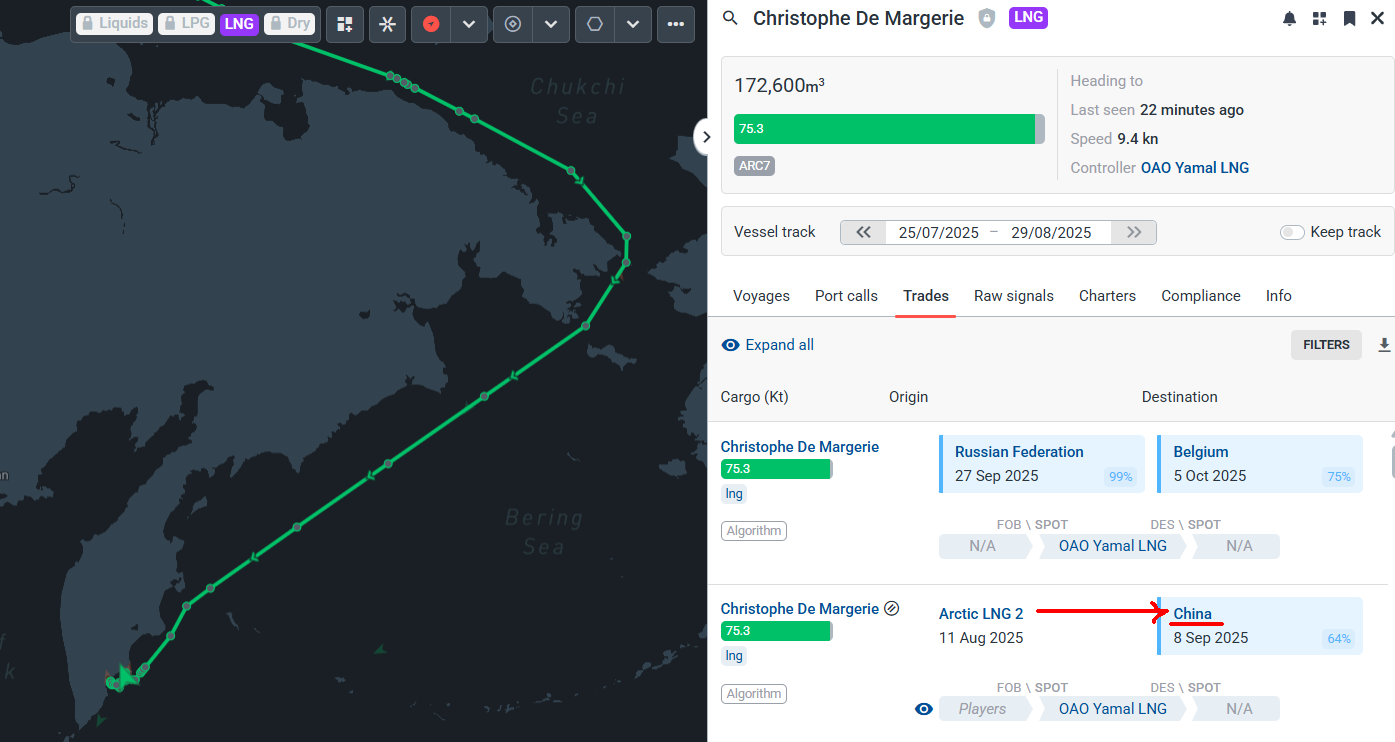

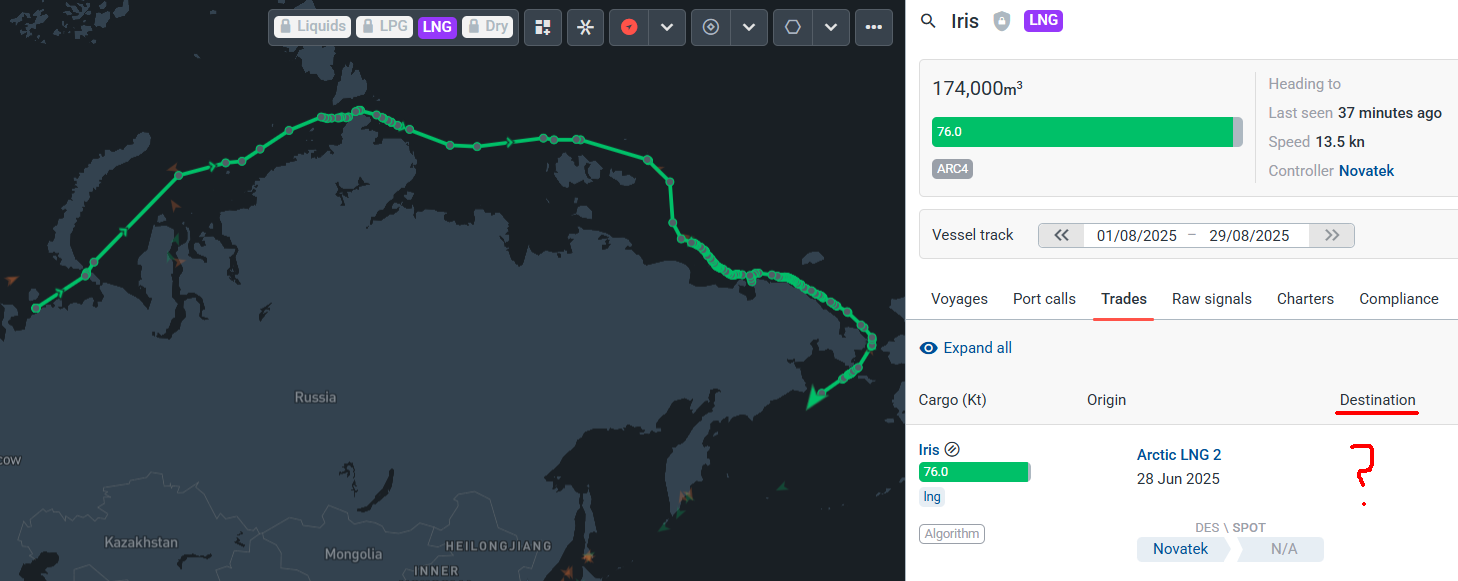

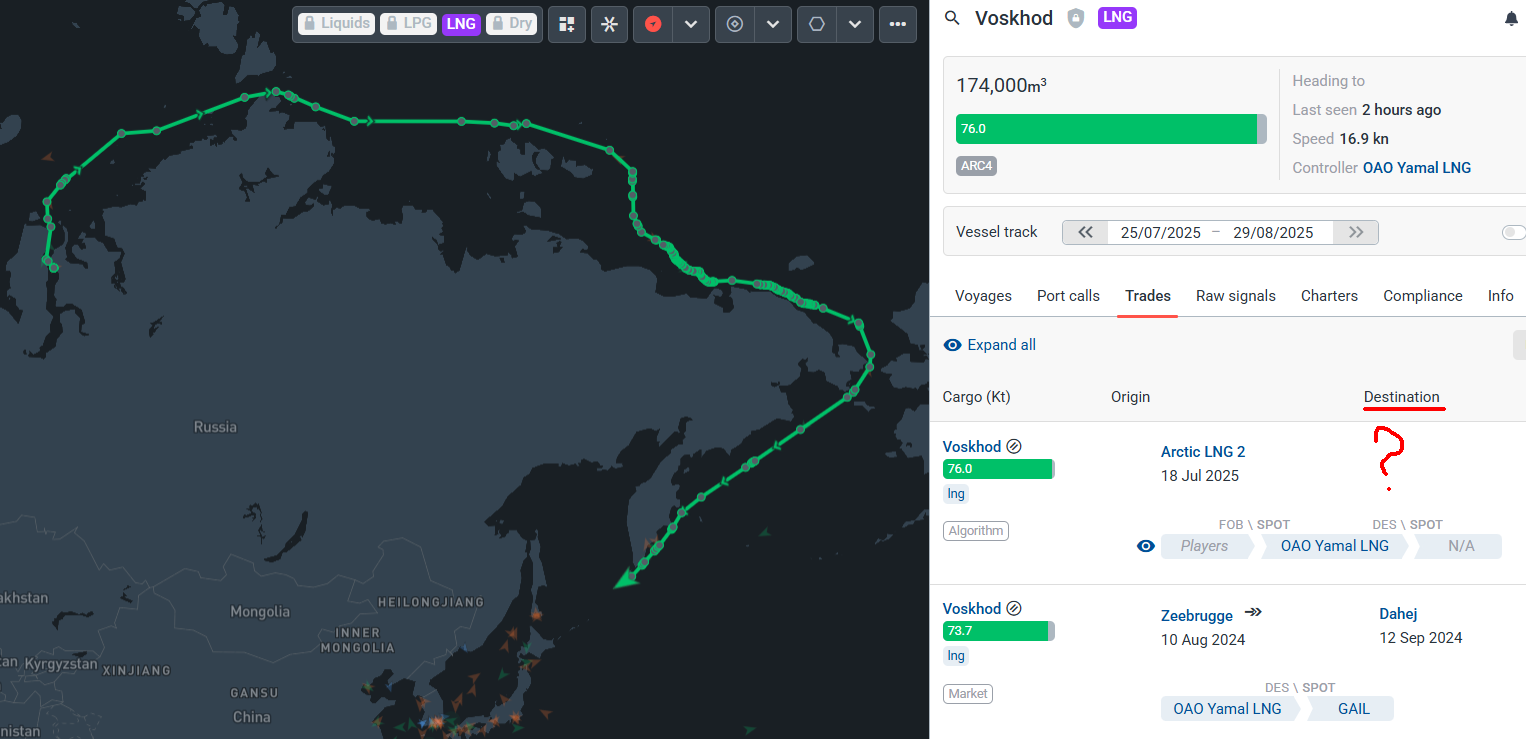

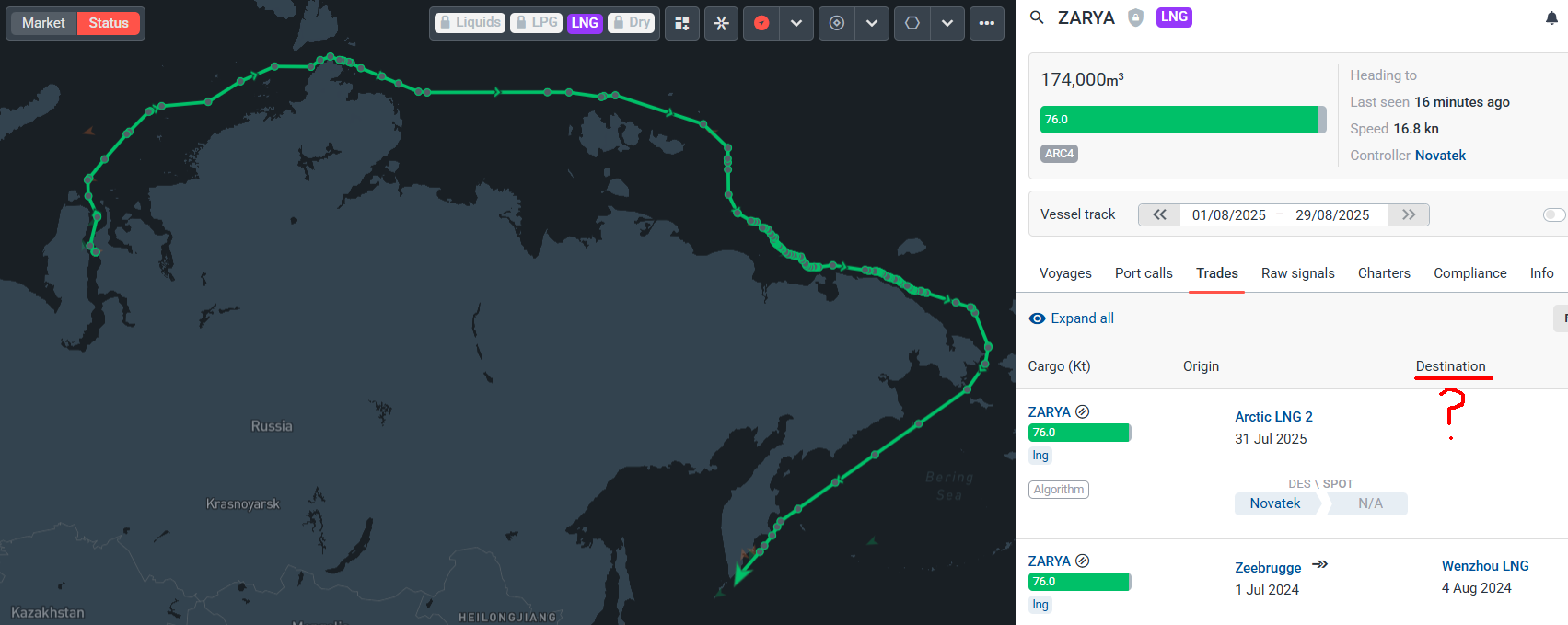

The big news in the LNG world this week was a cargo from Novatek’s heavily sanctioned Arctic-LNG 2 project discharging at a port in southern China.

The Arctic Mulan vessel loaded up from the Kamchatka trans-shipment facility in Russia’s Far East in June, before docking at PipeChina’s Beihai LNG terminal in the Guangxi Autonomous Region yesterday morning.

The timing was noteworthy: President Vladimir Putin will be making a rare trip outside of Russia to attend a high-level summit in the Chinese port city of Tianjin, which runs from Sunday through Tuesday. Cue a rehash of this classic meme:

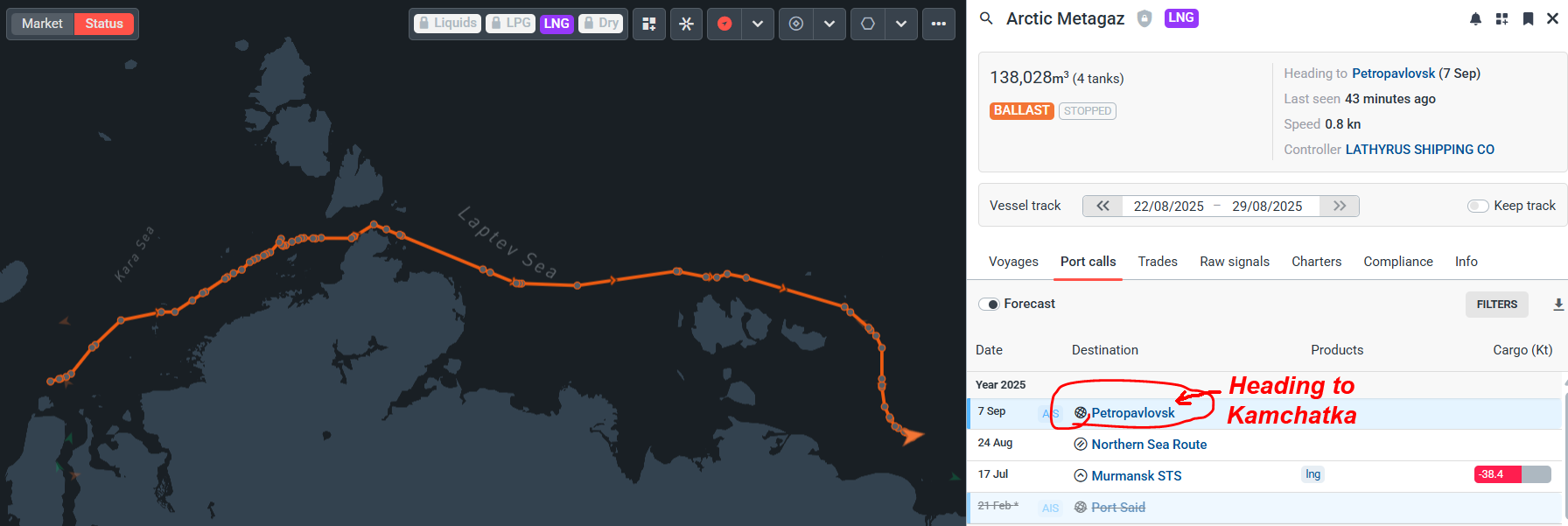

Russian LNG carrier movements are carefully choreographed. When Putin met Trump in Alaska, there was a flurry of activity as vessels that had idled for months suddenly set sail for Asia.

Currently, at least six vessels are traversing the Northern Sea Route either laden with Arctic 2 molecules or signalling to load up with sanctioned LNG from Kamchatka.

Maps and info from Kpler

Until now, none had unloaded their forbidden cargo; the threat of sanctions deterred buyers. With PipeChina apparently breaking the embargo, the question is whether US authorities will enforce the sanctions regime imposed against Russia during the previous Biden administration.

At the time of publication, neither the US State Department nor the White House had responded publicly to the sanctions breach.

Inaction is a signal: US sanctions are no longer water tight, but discretionary. The Trump administration might turn a blind eye, especially if it fits his current negotiating tactics (which include offering coveted American liquefaction technology to Russia in exchange for a Ukraine peace deal – make of that what you will).

The upshot? Don’t be surprised if Russian LNG cargoes start discharging at ports across Asia and even Europe this winter, before the EU ban on Russian energy imports comes into force in 2027.

The near-term impact is not massive, but it could “eventually” mean “30 bcm of LNG coming back to the market to add up to the pile of LNG under construction”, according to expert analyst Anne-Sophie Corbeau.

Level up your market insight for less: subscribe to Energy Flux with a time-limited discount (half-price Gastech special)

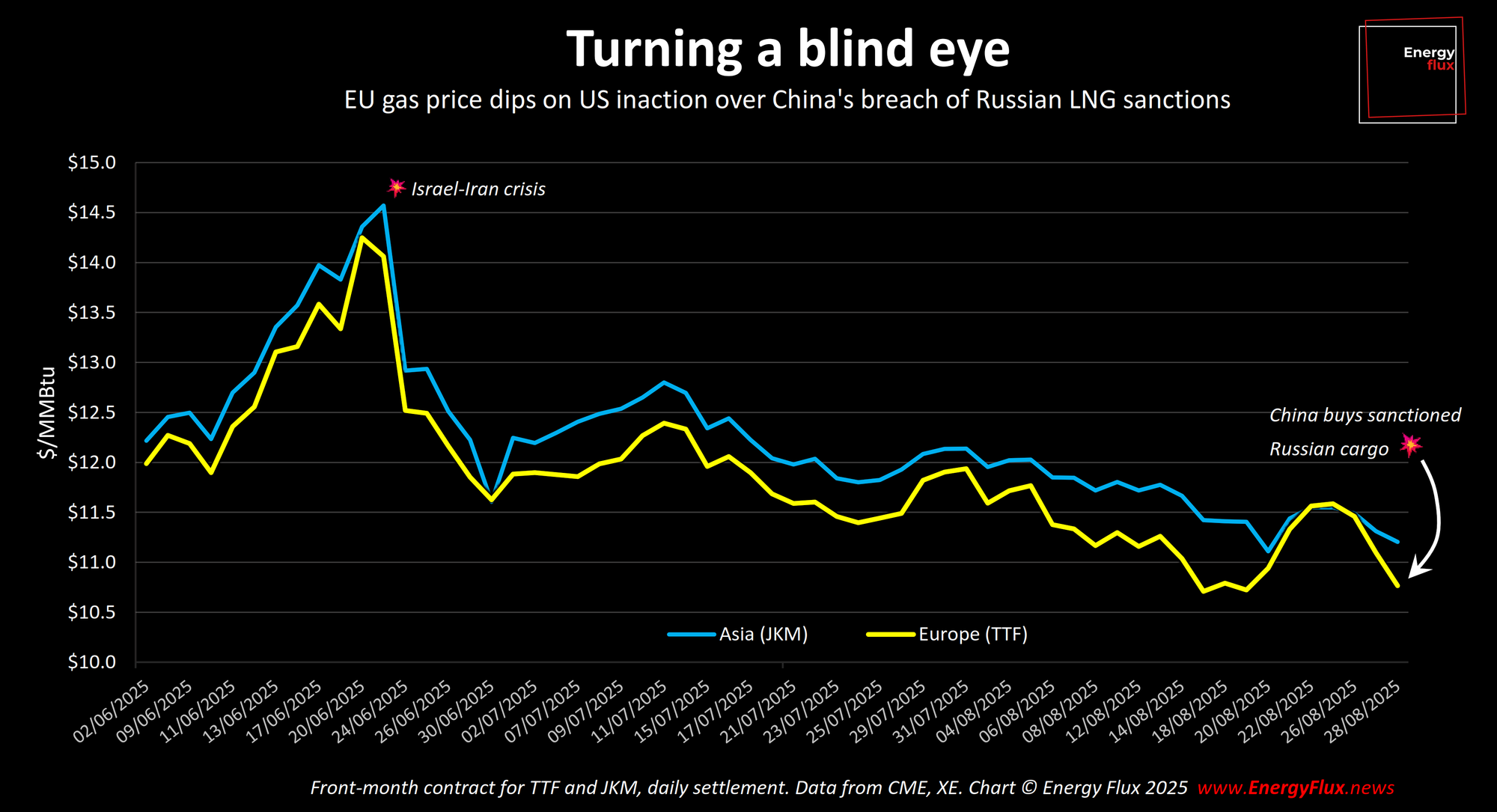

Muted price impact

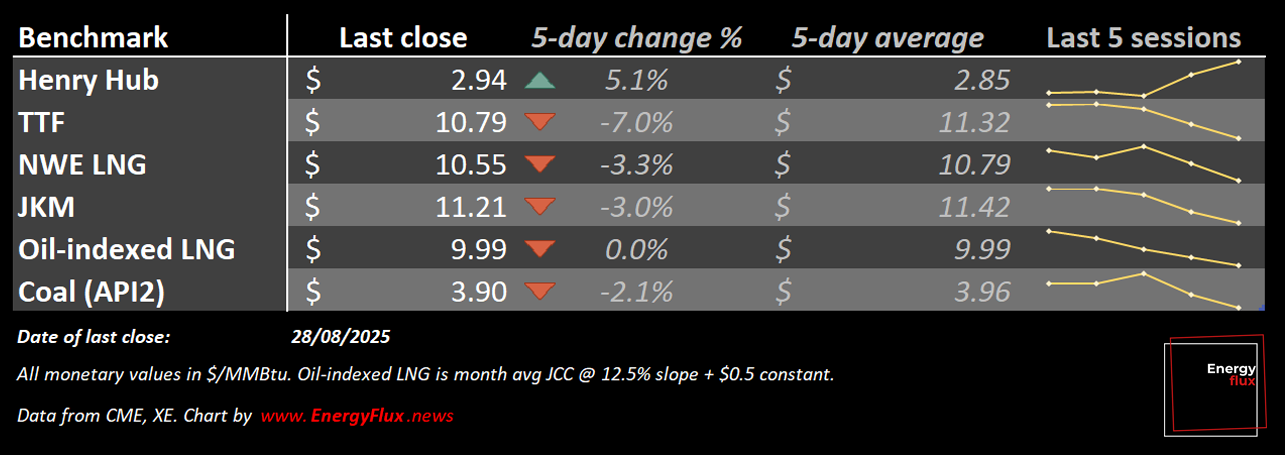

Dutch TTF, the European gas benchmark, fell <3% on the news of illicit Russian cargoes leaking into the market. Sep-25, the front month contract, settled at €31.70/MWh on Thursday.

It is a wonder that TTF has not already crashed through the €30/MWh support level. Only European restocking, scarcity narratives and geopolitical risk premia have kept prices inflated above fair value; the big question is for how long that floor can hold under the weight of excess supply.

The fate of Russian LNG, while of geopolitical significance, will not significantly alter the winter gas market balance. This week’s Chart Deck takes a microscope to the factors moving the needle. These include:

- Record-breaking global LNG supply surge outstripping demand growth

- China, south-east Asia and Latin America LNG imports surprising to the downside

- Investment funds shorting TTF and cutting directional bets to a 16-month low

- Divergent commercial hedging and discretionary exposure by physical players signalling neutral/soft

… and lots more besides. All of the above are reflected in the only metrics that matter:

- The Energy Flux TTF Sentiment Tracker and upgraded TTF Risk Model (v2.1), both of which point south 📉

Did I hear you say LNG deluge? Let’s dive in! (sorry)

Need access? Use GASTECH25 for half-price discount.

💥 Article stats: 2,500 words, 15-min reading time, 20+ charts and graphs

Member discussion: When the dam breaks

Read what members are saying. Subscribe to join the conversation.