Asia’s LNG demand: reality check

Shell’s 2026 Outlook leans harder than ever on stratospheric Asian demand to justify a new wave of LNG investment. But post-Hormuz, the data and policy responses all lean the other way.

Oil major Shell this week released its annual LNG Outlook, one of the most closely watched forward views in the global gas market. This year it recasts the long-anticipated supply glut as a temporary dip on the way to renewed tightness. The whole manoeuvre rests on one assumption: a surge in Asian demand in the early 2030s. But the demand trajectory in growth-engine markets, as well as policy responses to the Hormuz crisis, weaken that assumption.

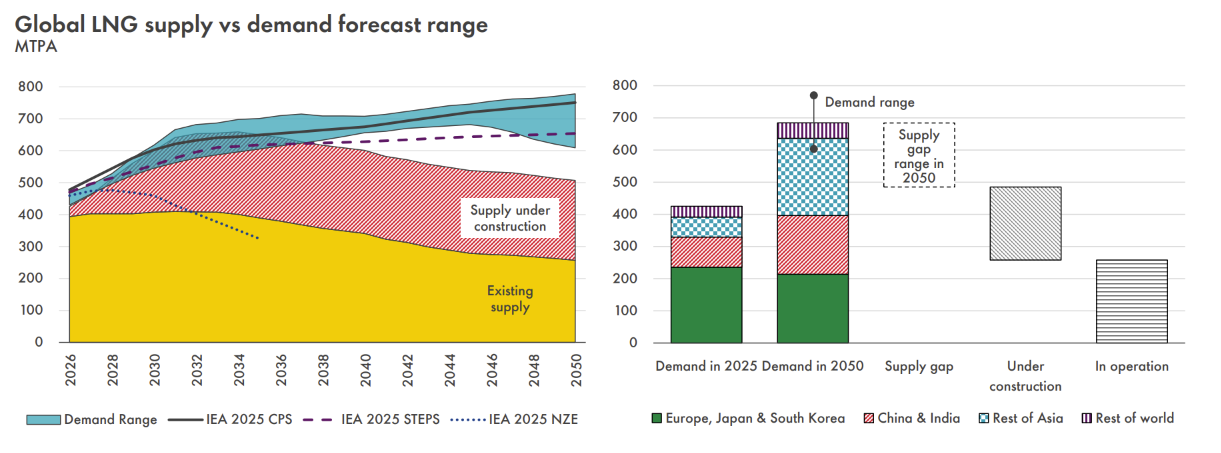

One chart in the Outlook is studied more closely than the rest: Shell’s global LNG supply-demand projection. It is the closest thing the industry has to a shared view of whether the world needs more export capacity, how much, and by when. If the demand range sits above the supply line, it sends a clear message to capital markets: invest in new LNG plants.

This year’s message is one of continuity through disruption. According to Shell, the world’s biggest publicly traded portfolio player, LNG remains “a core pillar of the global energy system,” its growth “driven by Asian economic growth and intensifying energy security risks.” The Outlook presents three shocks in six years as stress tests the market passed: the pandemic, the war in Ukraine, and now the Hormuz crisis in the Middle East.

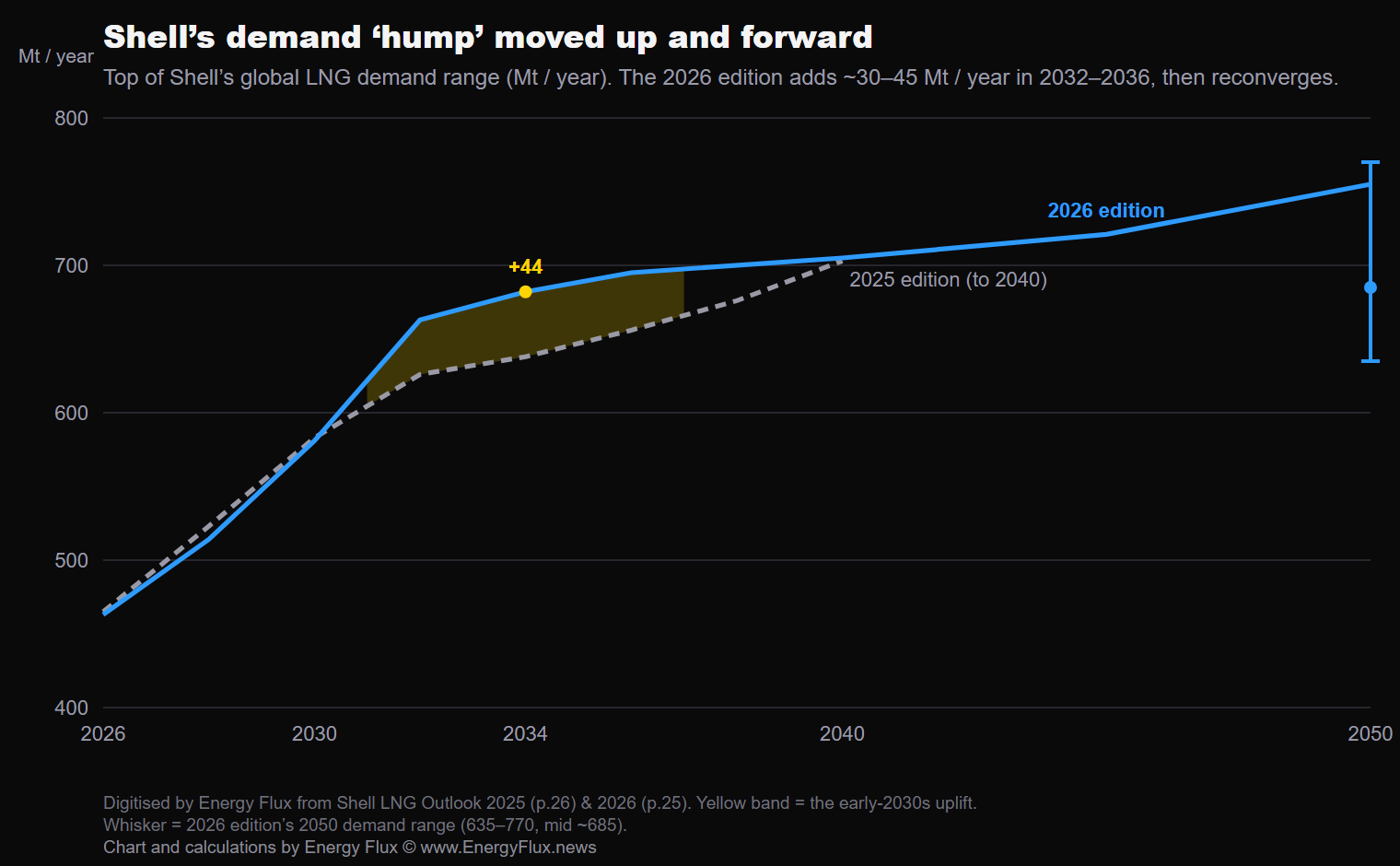

The headline number reaches further than before. For the first time it extends to 2050, and puts global LNG demand at around 685 million tonnes per annum (mtpa) by then, roughly 60% above 2025. Beneath that sits a “structural supply gap in 2050”: a ~200 mtpa wedge of future demand that sanctioned projects do not yet cover and which, in Shell’s telling, can only be filled by more liquefaction investment.

Almost all of that growth comes from Asian economies. Shell points to economic growth, urbanisation, and domestic production declines as the drivers. This is contingent upon a massive >140 mtpa infrastructure rollout which, as regular Energy Flux readers will recall, is highly unlikely to materialise (see Asia’s LNG bottleneck for a two-part Deep Dive into regasification constraints).

The hump that has to hold

Leaving aside the regas capacity issue, there is a more pressing question: post-Hormuz, is Asia both willing and able to buy up all the new LNG supply that is on the horizon?

Before the 2026 Middle East crisis, the dominant story in LNG was a coming glut: a wall of new supply from the United States and Qatar arriving between 2026 and 2030, outrunning demand and pushing prices down. The question was when the two lines would cross, with looser market conditions expected to drag prices below the affordability threshold for price-sensitive economies.

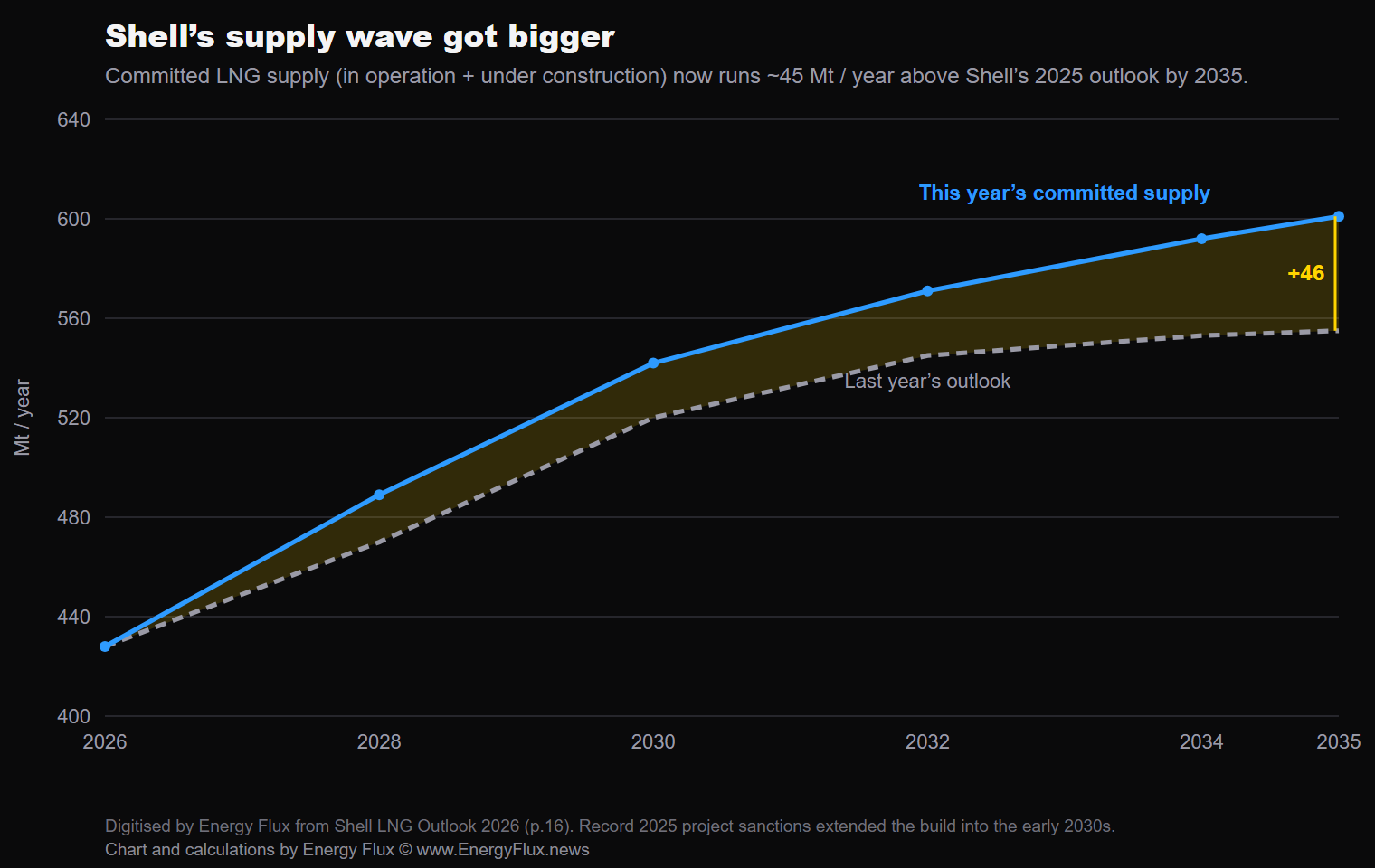

Shell’s 2026 edition does two things to that picture.

First, the supply wave got bigger. A record run of LNG project final investment decisions (FIDs) in 2025 pushed committed supply (operational plus under construction) well above what Shell projected a year ago.

By the mid-2030s, Shell now shows roughly 46 mtpa more committed supply than in its 2025 Outlook. More supply, arriving later. On its own, that deepens the glut rather than resolving it.

Second, in the 2026 edition, the demand line rose to meet it. Compared to last year, the demand range for 2030 and 2040 is essentially unchanged. What changes is the shape in between. A new bulge appears across the early 2030s, adding roughly ~44 mtpa of extra demand at its peak in 2033–34, before the two editions converge.

An early-2030s lift in demand is precisely what is needed to absorb a late-2020s glut. Raise the demand line in the years when the surplus lands, and an oversupply becomes a temporary dip before a renewed shortage justifies the next wave of liquefaction investment.

Shell does not dispute the surplus. In its view, an early-2030s demand surge turns it into a passing dip, and the shortage on the far side becomes the reason to keep building.

This thesis rests entirely on that surge in Asian LNG demand. Will it show up?

💥 Article stats: 3,500 words, 14-min reading time, 20 interactive charts & graphs

Below the paywall, we test the demand hump against seventeen years of cargo data and the choices every major importer has made since the Hormuz crisis.

The question is not whether Asia still needs gas. It is whether Asia is positioned to mop up the surplus fast enough to rescue the next wave of LNG investment.

The picture that emerges challenges the growth narrative that capital markets are prone to believe.

Member discussion: Asia’s LNG demand: reality check

Read what members are saying. Subscribe to join the conversation.