War vs. Glut: The Great LNG Reckoning

War shut in one of the world’s most critical export arteries. The long-promised supply wave is finally arriving. Which force wins, when, and by how much? Our new scenario data model brings clarity to the confusion.

The global LNG market has entered a phase of extreme uncertainty where outdated narratives go to die.

For the last 18 months or so, the consensus trade was simple: a wall of new supply was coming. The United States, Canada and Qatar would flood the market, loosen balances and drag prices lower. Then war arrived, the Strait of Hormuz slammed shut, two Qatari trains were blown up, and that clean, comforting story of abundance collapsed under the weight of a destabilising global reality.

Now the market is being asked to price two opposing truths at once.

On one side sits an extraordinary wartime supply shock, with Gulf exports constrained and uncertainty hanging over every vessel movement, repair schedule and diplomatic headline. On the other sits a vast queue of LNG projects that still promises to reshape global gas balances, albeit on capital-intensive infrastructure timelines rather than social media timelines.

That tension now defines the market. So we built a tool to measure it.

Today, Energy Flux launches the Hormuz Closure LNG Supply Impact Model: a premium scenario engine that allows readers to quantify the collision between lost Middle East supply and incoming global LNG capacity.

The model comes with pre-loaded assumptions that provide insightful conclusions in their own right. But the true value lies in the model’s interactive functions. Users can input their own assumptions, intelligence and market judgement to generate unique LNG supply projections.

The Base Case: structurally tight until end-2028

Start with the default assumptions and the conclusions are rather stark.

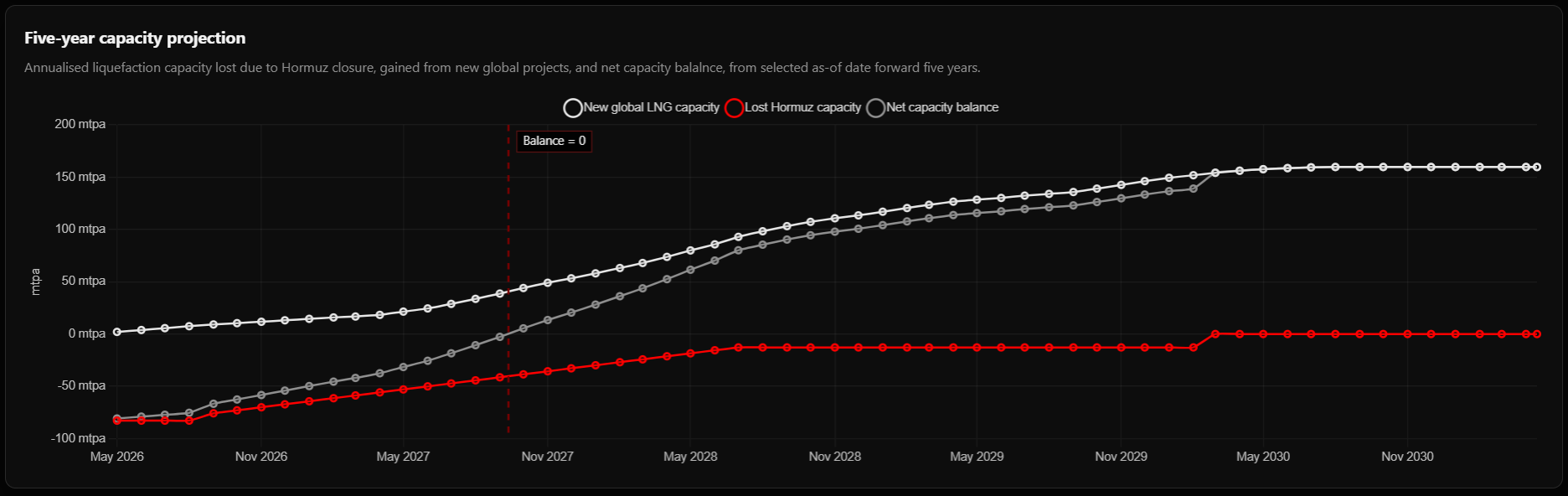

Under the Energy Flux base case, Hormuz only partially reopens in September, after which Middle East LNG transits gradually recover towards full flows in mid-2028. The two damaged Qatari liquefaction trains remain offline for four years, and new LNG projects continue to ramp at a realistic rather than miraculous pace.

Result: the supply hole is not repaired quickly.

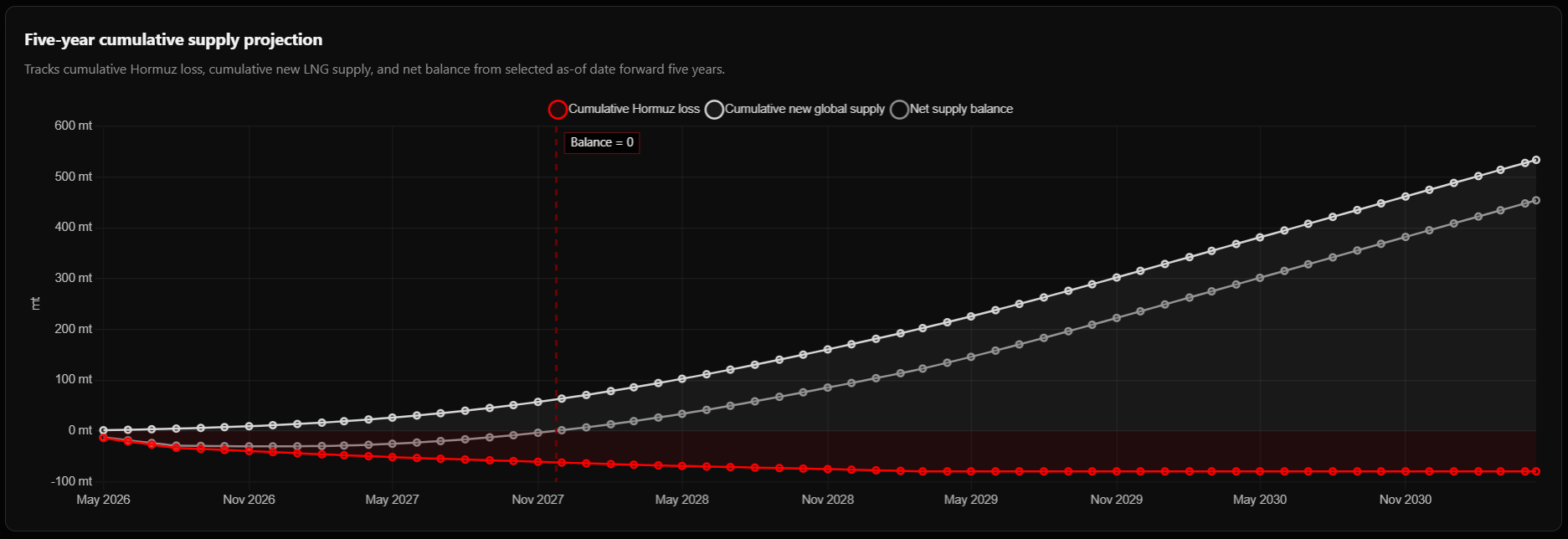

The model indicates that new global LNG capacity additions do not offset lost Hormuz-dependent capacity until September 2027. That is the point at which new non-Hormuz LNG capacity additions finally match the annualised capacity removed from the system.

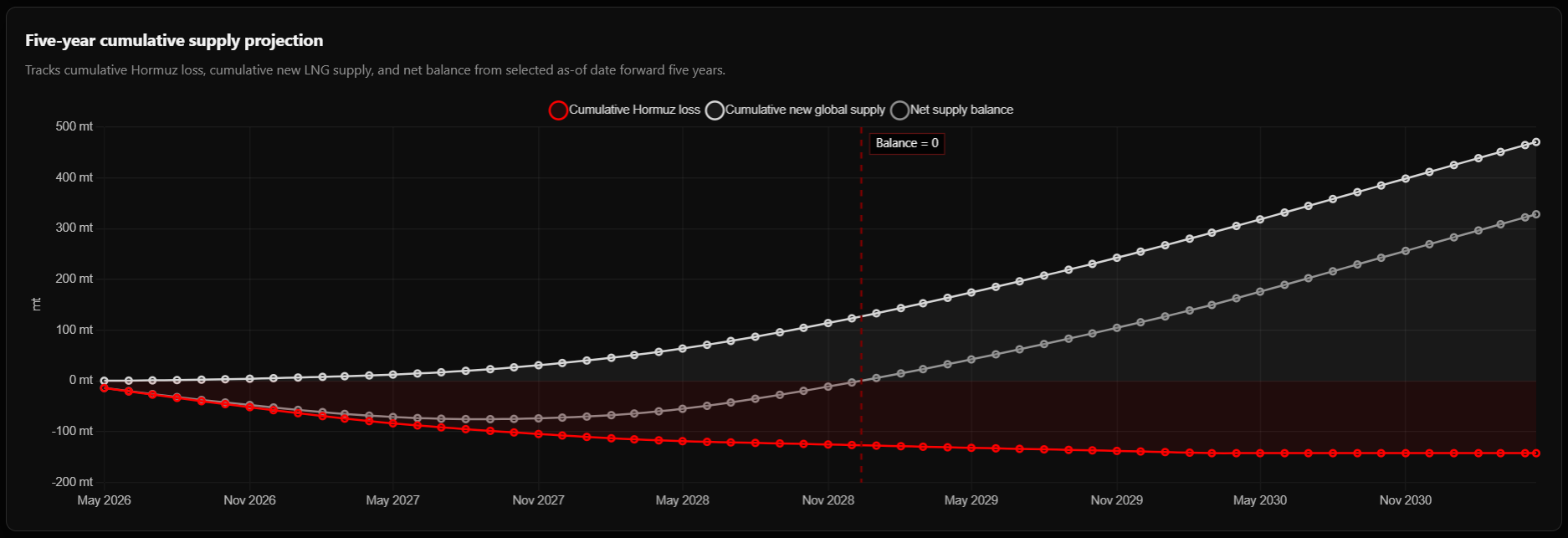

That sounds reassuring until you look at cumulative volumes. Markets do not consume nameplate capacity; they consume molecules. And cumulative lost supply compounds every day the disruption persists.

Roughly six weeks into the conflict, the physical shortfall already runs to more than 10 million tonnes. If current conditions drag into winter, the missing volume becomes systemically meaningful: almost 60 mt, or more than 13% of total worldwide LNG trade in 2025, by December 2026.

If disruption endures per the Base Case assumptions, the cumulative volume supply deficit stretches almost until the end of the decade. Assuming a 10% resumption of Hormuz flows and gradual recovery thereafter, cumulative supply from new LNG project additions since 1 March 2026 would offset cumulative lost Middle East LNG supply volumes in December 2028.

This is the part most commentary misses: even when replacement capacity starts arriving, it first has to dig the market out of the crater that has been deepening every day since the US and Israel started their joint attacks on Iran.

The optimistic take: a slow reversal of misfortune

The conclusions above are based on assumptions that could quickly be overtaken by events – which is why the Hormuz Closure LNG Supply Impact Model was designed to be adapted by users based on their reading of the highly fluid situation in the Middle East.

For example, if:

✅ Hormuz transits recover to 80% by August 2026, and to 100% by mid-2027

✅ The damaged Ras Laffan trains are repaired within three years

✅ The entire global LNG supply wave is accelerated by six months

➡️ then the picture changes dramatically.

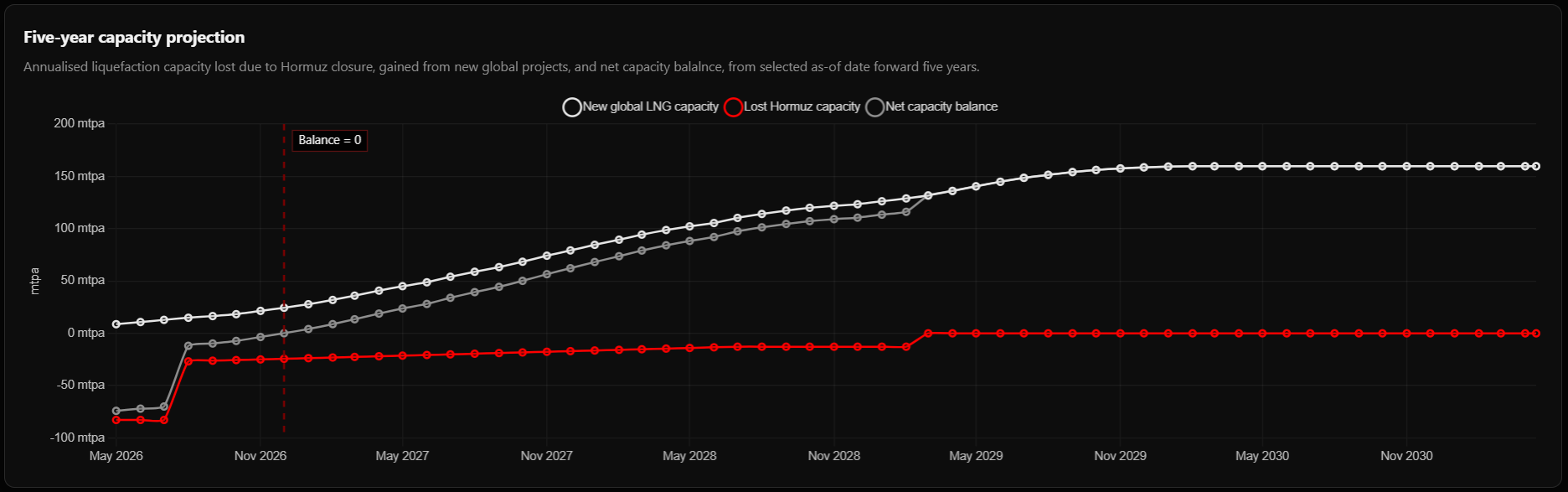

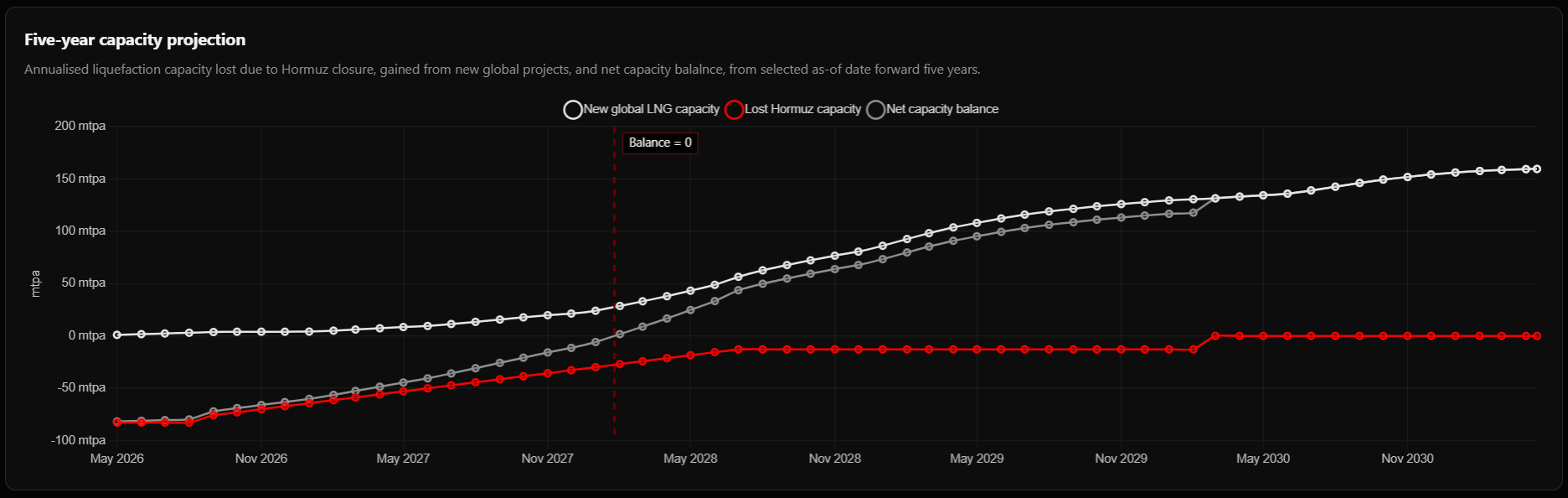

New capacity additions would replace lost Hormuz-dependent liquefaction as early as end-November 2026…

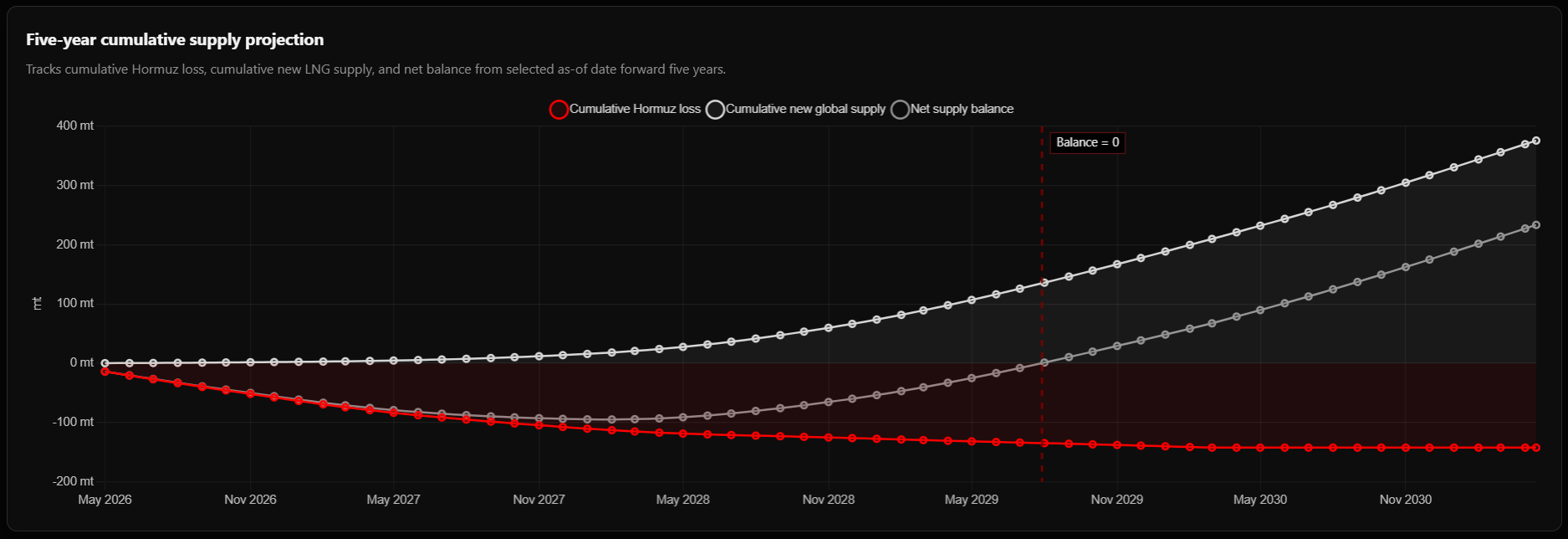

… and the cumulative physical supply loss from Hormuz closure could be completely eliminated by October 2027.

The divergence is substantial: in this more optimistic scenario, lost capacity would be replaced by new additions 10 months earlier than in the Base Case, and cumulative lost volumes would be fully replaced a full 14 months earlier.

This highlights the heightened sensitivity of LNG supply to ongoing diplomatic efforts, the double-blockade of Hormuz, and the threat of resumed conflict in this contested waterway.

The supply wave cometh?

The divergent modelling outcomes also demonstrate the market’s sensitivity to the timing of new LNG projects. While Hormuz is the critical factor determining near-term market balances, the coming supply wave is so big it has the clear potential to replace Middle Eastern supply altogether.

Plaquemines is already shipping hundreds of commissioning cargoes. LNG Canada is moving toward steadier utilisation after early technical friction. Golden Pass, Corpus Christi Stage 3 and others remain key pillars of the next growth cycle.

But none of that means the market is suddenly comfortable. Projects ramp in phases, trains can slip, utilisation rises slowly, feedgas constraints emerge. Commissioning cargoes make headlines but do not instantly rebalance the planet.

If these projects can accelerate their deployment, the market will rebalance much sooner. But if there are widespread delays (which users can model by adjusting the Global LNG Ramp Pace Shift input variable), then the optimism depicted above becomes illusory.

For example, if the entire global LNG supply wave is delayed by nine months due to labour shortages and materials cost inflation – a very real possible outcome of the US-Iran war – then lost LNG capacity will not be replaced until January 2028…

… and the LNG market would not rebalance until mid-2029.

Meanwhile, the disruption side of the ledger is enormous.

Around 83 mtpa of nameplate capacity in Qatar and the UAE sits inside the Hormuz risk envelope. Included within that is 12.8 mtpa of Qatari liquefaction capacity damaged in the March strikes, with a multi-year repair timeline assumed in the base case.

So yes, new supply is arriving. But whether it will arrive fast enough to erase a war is, at best, highly debatable. And all the while, the supply deficit is deepening is day by day, and all sides in the conflict are entrenching their positions.

The thick fog of an unwinnable war

After the failure of Friday’s peace talks, the shaky ceasefire between the US, Israel and Iran looks set to collapse at any moment. On Monday 13 April, the Trump administration imposed its own embargo on vessels transiting the Strait of Hormuz to access Iranian ports, in an attempt to starve Tehran of oil revenue.

Highly provocative towards China, this new blockade raises myriad questions around enforceability and credibility. Will US warships really open fire on China-bound oil tankers laden with Iranian crude? Having started this maddening and unwinnable war, will the US finally acknowledge the untenability of its position with a grand capitulation? Or will Washington make another move to maintain pressure and save face against an adversary that has proven surprisingly tenacious in the face of unprecedented aerial bombardment?

This wild game of brinkmanship is throwing into stark relief the many ‘known unknowns’ circling Hormuz and the future of Gulf energy exports. In this fog-of-war market, the only certainty is low information, high stakes, and constant narrative whiplash.

Until 1 March 2026, it seemed that the long-anticipated global LNG supply wave was finally about to break, only for a poorly-planned geopolitical war of choice to scupper that outlook. Overnight, the dominant narrative flipped from ‘LNG glut incoming’ to ‘unprecedented LNG supply shock’, leaving many observers dizzy and confused.

Faced with diametrically opposed ‘structural supply glut’ and ‘worst-case scenario supply shock’ realities, the number one question that Energy Flux readers have been asking is: how far, and how soon, can new global supply additions offset lost Hormuz volumes?

The Hormuz Closure LNG Supply Impact Model aims to answer that question by giving readers a disciplined framework for testing scenarios. Change the assumptions, watch the supply path retrace, and understand which variables matter the most.

What the tool lets you model

The engine comes pre-loaded with an Energy Flux base case, but it is built to be challenged.

Users can adjust Middle East disruption variables:

- Hormuz partial reopening date

- Percentage of flows restored after reopening

- Hormuz final full reopening date

- Inclusion or exclusion of Oman in the disruption baseline

- Repair timing for damaged Ras Laffan Trains 4 and 6

- Qatar North Field East first LNG timing

- The interaction between reopening logistics and stranded Qatari capacity

Users can also rework core global LNG supply wave variables:

- Project-by-project edits

- Nameplate capacity changes

- First LNG dates

- Full-capacity ramp dates

- Risk classifications

- Ramp profiles

- Global acceleration or delay factors applied across the global project queue

In short: you can model your own market, not ours.

⚙️ If you believe diplomacy restores 80% of LNG flows by August, model it.

⚙️ If you think the US LNG construction wave hits a six-month delay, model it.

⚙️ If you think Qatar recovers much faster than advertised, model it.

⚙️ If you think war keeps Hormuz closed for years and everything slips, model that too.

Why this matters now

The geopolitical backdrop remains almost absurdly unstable.

Ceasefires are partial at best, second-order threats are multiplying, and Washington is improvising coercive measures with unclear credibility. Tehran remains damaged but far from broken. China’s role looms over maritime enforcement. Leaders talk of peace in one breath and destructive threats in the next. Every actor is posturing, none is fully in control, and energy markets are forced to price a situation that nobody fully understands.

The old narrative of ‘LNG glut incoming’ has not vanished. It has collided with ‘historic supply shock’.

Both forces are live. Neither can be understood in isolation. That is precisely why this tool matters.

A clarion-call for clarity

The delta of uncertainty is so great that it creates space for motivated reasoning. Anyone with an opinion or agenda can influence how people think about what’s happening in the LNG space based on shaky assumptions, or worse.

The LNG market does not need louder opinions. It needs better frameworks.

The Hormuz Closure LNG Supply Impact Model is designed to do exactly that: turn chaos into concrete scenarios, convert narratives into numbers, and help serious market participants think more clearly at the moment clarity is in shortest supply.

The base case is nuanced, and slightly provocative. Whether you take a more optimistic or pessimistic line, your assumptions can now be modelled to visualise how the supply side of the global LNG ledger might evolve from here.

Subscribers can access the model right now on the Energy Flux platform. Just click here, log in, and stress-test your view of the market to see when, where and how the market balances.

Seb Kennedy | Energy Flux | 15 April 2026

You read the Deep Dive. Now check out the model behind the analysis.

The Energy Flux Hormuz Closure LNG Supply Impact Model is available only to subscribers on the Deep Dive and Premium subscription tiers.

A paid subscription gives you access to a wealth of insights. Can you afford not to arm yourself with unique market-shaping knowledge at this critical moment in history?

Member discussion: War vs. Glut: The Great LNG Reckoning

Read what members are saying. Subscribe to join the conversation.