The Spread is Dead

Storage without a signal: the new political economy of Europe’s gas buffer

The economics of gas storage is simple: buy low in summer, sell high in winter to cover your costs, and pocket anything left over. That profit signal, the seasonal spread, determines the pace and volume of injections... except, Europe’s world-beating gas storage capacity has been operating on completely different rules for years now.

The clearest demonstration yet came late last week in the Netherlands.

At 13:12 on Friday 3 July, the Dutch competition regulator ACM published a key decision about third-party access to Grijpskerk, one of Western Europe’s largest underground gas stores that has failed to attract capacity bidders in a long-running open season.

The ruling barred NAM, the Shell–ExxonMobil joint venture, from making access to Grijpskerk conditional on users contributing to Groningen earthquake liabilities. At 15:40, state-owned Energie Beheer Nederland (EBN) booked the entire 15 TWh on offer and began injecting at around 125 GWh/day. By close of business, NAM had shut the open season. The 2.4 Bcm facility, which accounts for almost 20% of Dutch storage capacity but had sat empty since 1 April, was committed to filling within an afternoon.

Note what was absent from that sequence: a price signal.

Grijpskerk did not fill because the summer–winter spread suddenly recovered. It filled because regulatory intervention allowed a state company to sign up two hours later. The spread on the day was negative and had been all season. In the regulator’s own words, NAM had reported “no serious interest from the market” in filling the site at any point.

Here’s what it took to change that: an arbitration ruling against Shell and ExxonMobil to force open the neighbouring Norg storage site; two court defeats for NAM in June, plus a binding conduct rule; and a €21.6bn state credit line for EBN to go and buy the gas itself, of which ~€1bn is an outright subsidy the taxpayer will never recover.

All of that machinery, to do what the textbook says a positive €2 summer-winter spread would have done on its own.

The irony is that the Netherlands is the EU country that originally chose not to mandate storage refilling. It was the flagship of the market-led approach. That country now has all four of its storage sites being filled by the state: Norg since April after an arbitration ruling compelled NAM to open the site; Bergermeer, which the state has backstopped since the 2022 crisis; Alkmaar, where injections into a new 5 TWh state emergency stock began on 30 June; and now Grijpskerk.

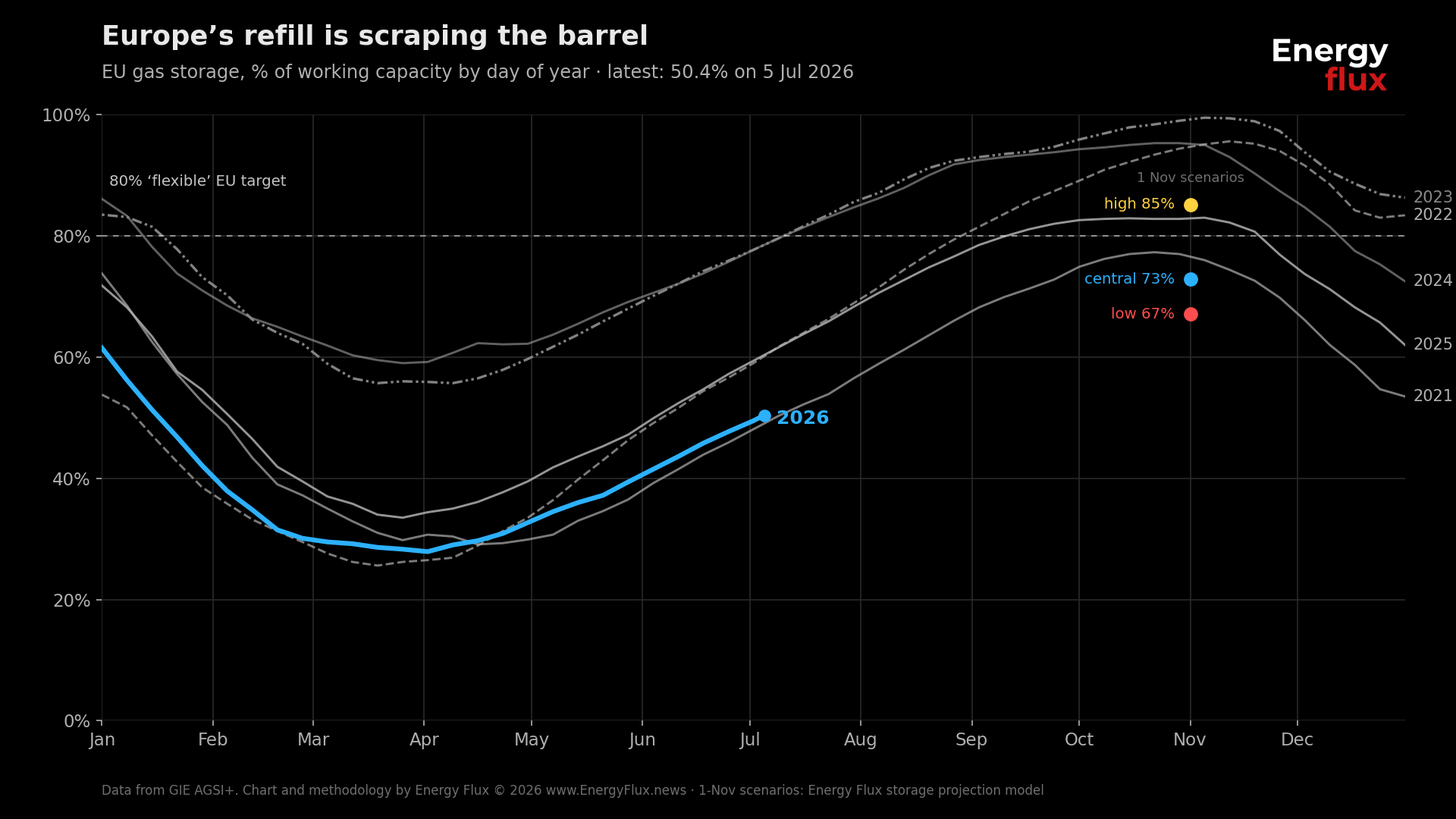

Meanwhile, the EU’s aggregate fill level crossed 50% on 4 July, a month later than every refill year since 2021, when the crisis-era low pushed the crossing back to 8 July. In the two semi-comfortable years (2023 and 2024), storage never dropped below 50% at all.

At 50.4%, Europe is tracking that crisis-era low, with roughly a third of total capacity still to inject before winter, into a forward curve that says storage loses money. At this rate, the Energy Flux EU gas storage model projects a 1 November fill level of 73% under its central case:

Fighting over the wrong thing

The Grijpskerk saga is a microcosm of the wider regulatory mission creep that’s transformed how Europe’s gas storage capacity is managed since 2022, when the loss of Russian pipeline gas put European energy security on a war footing.

The regulation that drives the restocking pace (and, by extension, winter price expectations) is due to expire next year. The gas industry is tearing itself apart over what, if anything, should replace it. And all the while, the clock is ticking: whatever replaces the regulation must be legislated before the 2028 filling season, by institutions and stakeholders that struggle to see eye-to-eye.

Eurogas, the gas industry trade body, wants the regulation to lapse, arguing that EU filling obligations distort the very price signals that should drive storage. Brussels points the finger at national policies for flattening the summer-winter spread. Some in industry are calling for a strategic reserve or a new scheme to compensate storage for insurance value.

The debate centres on ensuring caverns get filled and get paid for services not covered by the market price, while preserving a functioning spread.

But here’s the thing: the summer-winter spread, the signal that’s supposedly crucial to Europe’s winter gas restocking effort, barely matters these days.

New research by Energy Flux reveals how little of Europe’s storage still fills in response to the summer–winter spread. Nine years of facility-level injection data reveal that injections stopped tracking the spread long ago; and the regulatory easing of 2025 exposed what actually fills the tank once the binding EU target is relaxed.

In this Deep Dive:

- How national policies, not the market, now refill EU gas storage — and how six divergent national systems drive sharply different outcomes

- Whether a tradeable seasonal price signal can be revived by deregulating the EU mandate further

- Why only 5% of Europe’s storage capacity still responds to the summer–winter spread: a single number that shows how far policy has displaced the market

- The relative cost of storing gas under each member state’s regulatory approach, and who ultimately foots the bill

- A short-list of storage companies that now control Europe’s winter buffer

- An honest examination of a pressing question: does the row in Brussels over renewing the EU regulation matter at all?

💥 Article stats: 6,000 words, 25-min reading time, 5 charts, 1 table

The received wisdom on gas storage is wrong: the summer-winter spread stopped being the prime incentive for injections years ago.

This Deep Dive shows what replaced it: eighteen national policies, mapped against nine years of facility-level injection data, that decide which of Europe’s storage sites fill and which sit empty into winter.

If you procure gas for European industry, trade TTF, or manage gas exposure, it names the mechanisms, what each one costs, and the specific facilities where 2026’s refill effort will fail or succeed.

Credit card not an option? Need group access, or a corporate account?

We offer flexible subscription options to suit all needs

Member discussion: The Spread is Dead

Read what members are saying. Subscribe to join the conversation.