Will the €50 ceiling hold?

“After four months of paralysis, the relief is palpable. It may also be misleading. And it is almost certainly temporary.” – Energy Flux, 26 June 2026

Well, that didn’t last long.

Barely three weeks into a supposed two-month ceasefire, US missiles and Iranian drones are criss-crossing the Persian Gulf again. Iranian railway bridges, merchant vessels, and American military bases in Kuwait and Bahrain were all targeted in the last 48 hours.

Donald Trump this week declared the peace memorandum he signed in Versailles as “over”, after Iran struck ships transiting the Strait of Hormuz.

Among them was a fully-laden LNG carrier belonging to Nakilat, Qatar’s state-backed shipping company. The Al Rekayyat is awaiting salvage off the Omani coastline after its engine room took a direct hit and caught fire. Risk of explosion is said to be real but low.

Salvaging a bombed-out LNG carrier in an active warzone might prove easier than saving the ill-fated diplomatic process that Trump initiated in the most perfidious manner imaginable. Trust is at rock-bottom, and both sides have diametrically opposed objectives.

As Energy Flux has reported previously, whatever the original war aims might have been, the crux of the issue now is who gets to control the Strait of Hormuz. Never mind that this is a diminishing asset; the leverage it bestows today is too powerful, too existential, to be relinquished by either side.

Neither Washington nor Tehran have the political leeway to soften their red lines nor the means to achieve their maximalist objectives. So they thrash about in pursuit of leverage, any sort of bargaining chip that could give them a negotiating edge.

This cynical game locks energy markets into an endless loop of repricing on low-level kinetic exchanges, doveish overtures, uneasy standoffs, hawkish threats and carefully calibrated missile exchanges.

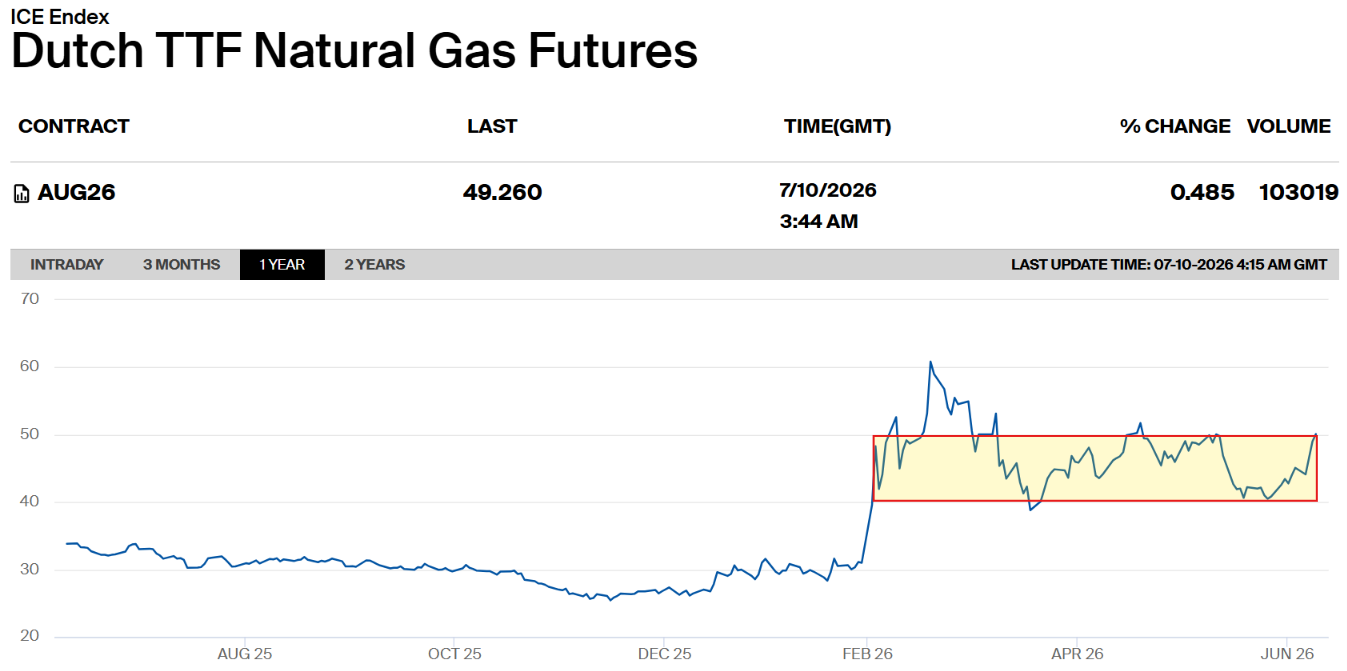

The cycle keeps the fear of full-throttle open warfare front and centre without (hopefully) ever pushing the region back into that hellish place. The result is a structural war premium that, in the case of the European gas market, manifests as a €40/MWh floor and €50/MWh ceiling.

That ceiling has been tested before, and it held. The front month contract on Dutch TTF, the European gas benchmark, yesterday settled at €50.102 – a seven-week high.

With Asian LNG demand showing tentative signs of revival this summer, will it hold again? Can Europe refill its depleted gas storage facilities without triggering an LNG price war? And what about the permabullish investment funds that have the means to propel TTF as high as their conviction takes them?

All of these crucial questions and more are addressed in this week’s 125-slide Chart Deck and subscriber-only market analysis.

💥 Article stats: 1,200 words, 5-min reading time, 125-slide downloadable Chart Deck (PDF, PPSX)

- Global Gas & LNG benchmarks — How are TTF, JKM and Henry Hub reacting to the latest Hormuz flare-up?

- TTF Sentiment Tracker & Risk Model — Funds are creeping back into length after weeks of selling. Conviction trade, or dead-cat bounce?

- TTF Value-at-Risk analysis — How much risk budget do funds have left to spend, and is the hidden ceiling still €50?

- The Storage-Speculation Nexus — Which contract along the curve are the funds really betting on? (Hint: it’s not the front month.)

- US-Asia LNG trade dynamics — Who is winning the EU-Asia tug-of-war for cargoes?

- Global LNG flows & supply modelling — If Hormuz stays shut, when does the ‘glut’ finally outrun the war? Our model has a date, and it’s further away than you think…

Credit card not an option? Need group access, or a corporate account?

We offer flexible subscription options to suit all needs

Member discussion: Will the €50 ceiling hold?

Read what members are saying. Subscribe to join the conversation.